Why European BOPP Isn’t the Answer for North American Converters to Hormuz Disruptions

Published on May 25, 2026

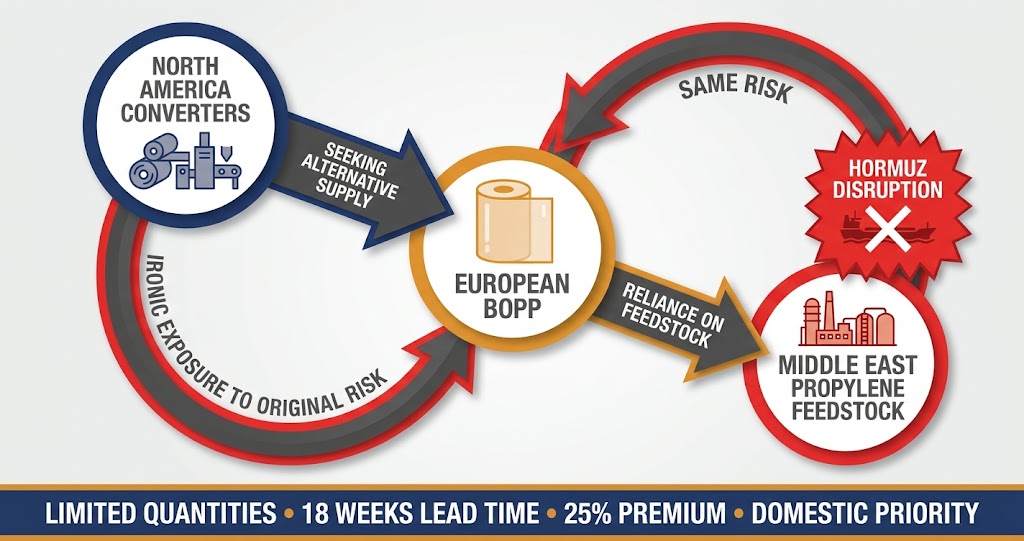

Your procurement team just found a European BOPP producer. Perfect timing—you need alternatives to Pakistan and India suppliers affected by Strait of Hormuz disruptions.

Then you get the email: “We can offer limited quantities. Priority to European customers. Lead time 16-18 weeks. Price 25% above your current Asian suppliers.”

European BOPP looked like the solution to Middle East shipping chaos. It’s not. Here’s why.

The feedstock squeeze: Why European producers can’t scale up

When Iran-USA/Israel tensions closed the Strait of Hormuz, North American converters looked for alternatives. European sources appeared attractive: Mediterranean shipping routes bypass Hormuz and Red Sea entirely, shorter Atlantic crossing, established quality.

What they discovered: European BOPP producers face the same Hormuz problem—just on the feedstock side instead of the shipping side.

Here’s what’s happening across Europe:

BOPP production requires propylene resin as feedstock. European propylene comes from two sources:

- Domestic naphtha crackers (limited capacity, high cost)

- Imported propylene from Middle East petrochemical complexes (UAE, Saudi Arabia, Qatar)

The Strait of Hormuz disruption cut off European access to low-cost Middle East propylene.

According to recent industry analysis, with oil and natural gas markets disrupted by the halt of shipping through the Strait of Hormuz, basic chemicals — such as ethylene and propylene, which go into plastics — have become increasingly uncompetitive to produce in Europe.

Producers across Europe are experiencing the same constraint. A Bulgarian producer explained: “We’re seeing growing demand from US customers wanting European-produced BOPP to avoid Hormuz shipping risks. But we’re facing propylene resin shortages ourselves because our suppliers in UAE and Saudi Arabia can’t ship through Hormuz economically.”

The cruel irony: North American converters are trying to escape Hormuz disruptions by sourcing European BOPP. European BOPP producers are constrained by Hormuz disruptions affecting their propylene feedstock.

European producers prioritize domestic sales—and higher margins

Even when European BOPP producers have material available, they’re not prioritizing North American exports.

Why Europeans serve domestic customers first:

- Higher margins: 12-18% premium over export pricing for local supply and shorter lead times

- EU “Made in Europe” policies: EU content requirements and sustainability standards prioritize domestic production

- Lower costs: Avoid transatlantic shipping ($8,000-12,000 per container), carbon border adjustment complexity, currency risk

- Captive demand: European packaging converters are under pressure from CPG brands to source EU-produced materials

The capacity reality: European chemical capacity is shrinking, not growing. Net capacity reduction announcements: Germany (-8 million tonnes), the Netherlands (-7 million tonnes), the UK (-4.2 million tonnes), France (-3.5 million tonnes).

The output of the EU27 chemical industry remains 10% below pre-crisis levels of 2014-2019.

European producers aren’t expanding to serve North American demand. They’re contracting and focusing on preserving European market share.

Eastern Europe: Limited capacity, same constraints

Eastern European producers (Bulgaria, Turkey, Romania) face similar pressures:

Feedstock dependency: Propylene still comes from Middle East via the Strait of Hormuz, creating the same supply constraint North American converters are trying to avoid.

Capacity utilization: Producers are running at 60-75% capacity—not because of lack of demand, but because of feedstock availability and cost constraints.

Export orientation shifting: Historically, Eastern European producers exported 40-50% of production. That’s declining as Western European demand captures more output at better margins.

Energy costs: While lower than Western Europe, Eastern European producers still face costs 2-3x higher than US Gulf Coast competitors.

What North American converters are experiencing

Real procurement scenarios from Q1-Q2 2026:

Scenario A: Converter contacts Eastern European BOPP producer in March 2026. Response: “We can offer 2 containers per month maximum. European customers have priority. Lead time 18 weeks. Price $1.72/lb landed vs your Pakistan supplier’s $1.52/lb.”

Scenario B: Converter negotiates with Turkish producer. Gets 4-month commitment. Three months in, producer invokes force majeure citing propylene feedstock shortage. Converter back to square one.

Scenario C: Converter locks in German BOPP supply. Then discovers German producer sourcing propylene from India, which imports aluminum from UAE, creating the same Hormuz exposure they were trying to avoid.

The pattern: European BOPP isn’t an escape from Hormuz risk. It’s Hormuz risk with higher costs and longer lead times.

The geographic diversification reality

Don’t confuse “different shipping route” with “different risk profile.” If European producers rely on Middle East propylene, you haven’t eliminated Hormuz exposure—you’ve just added complexity and cost.

True diversification requires:

Multiple source regions with different feedstock dependencies:

- China BOPP: Domestic propylene from coal-to-olefins (no Middle East dependency), Pacific shipping

- Indonesia/Thailand BOPP: Regional propylene sources, Pacific shipping

- Korea BOPP: Mix of domestic and Asian propylene, Pacific shipping

- Turkey BOPP: Some domestic propylene plus Mediterranean shipping access

Multiple shipping route options:

- Pacific routes (China, Indonesia, Thailand, Korea) → US West Coast

- Atlantic routes (Portugal, Turkey) → US East Coast

- Avoid over-concentration in any single chokepoint region

Pre-qualified alternatives across all regions: When Eastern European suppliers can’t deliver, Indonesia activates. When Pakistan faces shipping delays, China provides backup. When Turkey invokes force majeure, Korea covers the gap.

What procurement teams should understand

European BOPP made sense historically. Established producers. Reliable quality. Reasonable logistics. Before 2020, it was a solid sourcing strategy.

European BOPP makes less sense in 2026. Feedstock constraints, capacity decline, domestic market priority, and premium pricing mean limited availability for North American converters—exactly when you need alternatives most.

True diversification requires understanding entire supply chain—not just where the film is produced.

👉 Now Plastics sources BOPP from China, Korea, Indonesia, Thailand, Turkey, and Pakistan—each with different feedstock sources and shipping routes. When Hormuz disruptions constrained Pakistan and India supply, our customers shifted to Pacific-route alternatives within 48-72 hours. When European producers prioritize domestic sales or face propylene shortages, we have pre-qualified Asian alternatives ready to activate. True geographic diversification means understanding feedstock dependencies, not just where the film is produced. Contact us.

Analysis of European BOPP supply constraints for North American converters. For supply chain resilience strategies, see our series on tariff monitoring, geographic diversification, safety stock strategy, and Iran-USA/Israel conflict impacts.